March 29, 2022

2021 has been a high-octane year for mergers and acquisitions (M&As) in the FinTech world. The FinTech industry, which initially came to the fore on the promise of competitive disruption, has come through the ranks and has matured towards collaboration and consolidation. 2021 was a breakout year for M&As with well over 800 M&A deals, showcasing massive consolidation across key FinTech sectors such as Digital Banking, Payments, Buy Now Pay Later (BNPL), Lending, Wealth Management, Insurance, FinTech Infrastructure, and Decentralized Finance (DeFi).

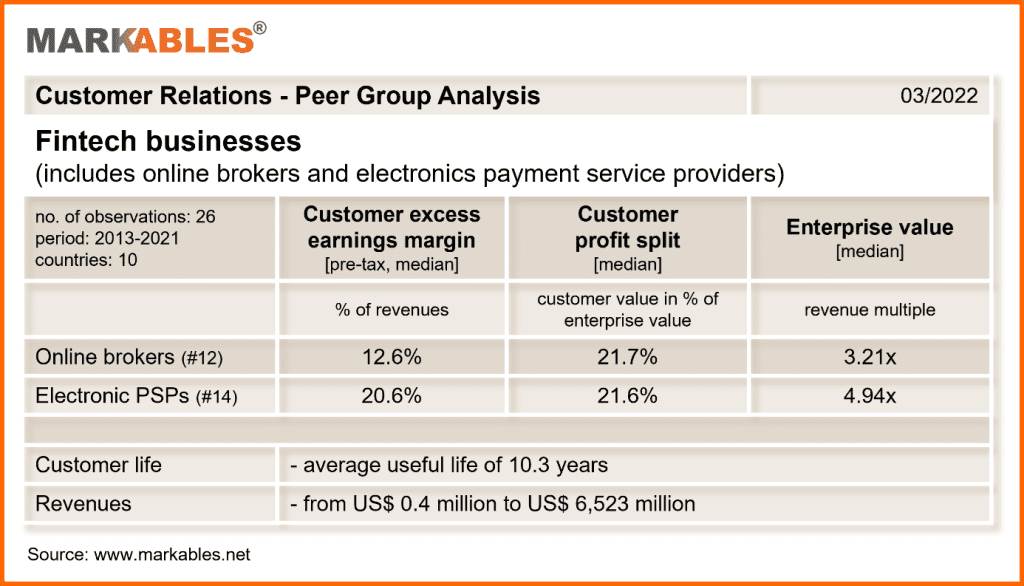

We have recently posted an analysis of the trademark intangible assets of FinTechs here. Accordingly, appropriate trademark royalty rates are 2.1% for online brokers on average, and 1.2% for payment services. Trademarks are typically short-lived and account for less than 5% of enterprise value. In this issue, we have a closer look at the customer relations of FinTechs.

One thing is obvious and does not come as a surprise. The true value of FinTechs lies in their customer relations (see table). All customer related valuations parameters are substantially higher than for trademarks. Excess margins of customer relations are 10x higher than trademark royalty rates, the share of customer value in enterprise value (customer profit split) is almost 10x higher, and the useful life of customer assets is some 30% longer than for trademarks.

Why is this? There are two reasons. First, technology enables FinTechs to know their customers and to install toolsets to retain them. Through agreements, through customized service and product offerings, through switching cost, and more. Second is scalability and margin per customer. Once acquired, each customer is “cheap” to service through technology, at no or very little additional cost. As a result, the profit margin of each additional customer is very high.

Customer margins for FinTech companies are substantial. The analysis shows that customer relations are more valuable for PSPs, than for online brokers. As average, we find margins of 20.6% on revenues for electronic payment service providers, and 12.6% for online brokers. There are several reasons for this difference:

As a result, PSPs have higher valuation multiples at enterprise level, and on the value of their customer relations. In contrast, we have seen that the brand name is more valuable for online brokers.

We will present technology-related comparable valuation data for the same sectors shortly. So please stay tuned …

Get relevant and robust market comps for your valuation within minutes.

Herrengasse 46a

6430 Schwyz / SZ

Switzerland